In my last blog, we talked about “what are voluntary benefits.” READ LAST BLOG

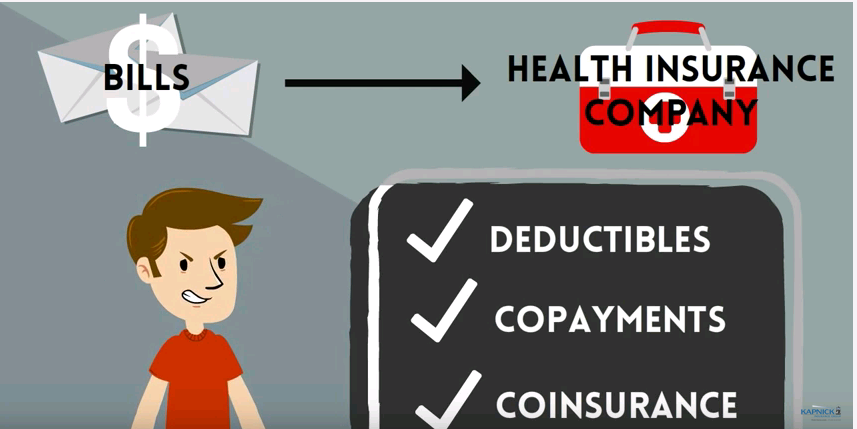

Now we are going to start discussing the first on the list of voluntary benefits: supplemental plans. These plans are designed to pay cash directly to the policyholder in the event of some specific illnesses or injuries. The various plans are designed with a list of benefits that will pay the policyholder either a large “lump-sum” benefit upon diagnosis, or a series of benefits based on what treatments the covered person goes through. The employee can use the money wherever he or she sees fit, whether their deductibles and copayments or their regular bills at home.

As I stated, the employee can use the benefits to help fill in whatever gaps they may have, like deductibles, copayments and coinsurance, or to simply help them pay their bills at home like mortgage or rent, car payments, and utility bills. These latter expenses are in many times the greater concern, because when they, their spouse or kids are getting medical treatments their income is likely being reduced due to missing work.

Quoted in many studies, 3 out of 5 bankruptcies are the result of medical expenses, while nearly 4 out of 5 of those households who filed for bankruptcy had health insurance. It isn’t the medical bills that cause them to go bankrupt, it’s the fact that 65% of America doesn’t have access to $1,000 in an emergency without borrowing it, according to a survey from Aflac*. Not surprisingly, this is even worse with the younger Millennials, and Generation Z. In Millennials, 62% surveyed have access to less than $1,000 in an emergency without borrowing it, and 28% have access to less than $500. For Generation Z, fully 84% have access to less than $1,000, and 49% have access to less than $500.

*Aflac 2016 Workforces Report - https://www.aflac.com/business/resources/aflac-workforces-report/default.aspx